What Is an Insurance Claim and How Is It Paid?

An insurance claim is a set of documents you file with the insurance company after an accident. If the accident is covered by your policy, the insurance company will cover your costs.

You can make insurance claims for damage to your car or home, injuries after an accident, medical checkups and life insurance benefits.

It can take a few weeks to a few years for the insurance company to pay your claim. The length of the claims process depends on the type and size of your claim.

Types of insurance claims

There are several different types of insurance claims.

The type of claim you need to file depends on your policies and what they cover.

Find Cheap Auto Insurance Quotes in Your Area

Auto accident claims

The most basic car insurance typically pays for property damage or injuries to others when you cause an accident.

If you have collision coverage, you can file a claim for damage to your car, even if you caused the crash. Comprehensive coverage pays for damage caused by something other than a collision. This can include fire, theft, falling objects and natural disasters.

Car insurance can also include uninsured and underinsured motorist coverage. This pays for damage or injuries if the at-fault driver doesn't have insurance or you're the victim of a hit-and-run.

Home insurance claim

Homeowners insurance covers the structure of your home, your belongings and injuries to guests in your home.

An insurance company will pay a homeowners claim if your policy covers the cause of the damage, like fire, theft or wind.

Homeowners insurance also includes additional living expenses coverage. This coverage pays for a rental home or hotel if damage to your home makes it an unsafe place to live.

Renters insurance claim

Renters insurance pays claims related to theft or damage to your belongings. It also covers personal liability for damage or injury and additional living expenses if you need to move temporarily.

Like homeowners insurance claims, renters insurance claims depend on the cause of damage, like fire, smoke or vandalism.

Health insurance claim

Your doctor's office generally handles health insurance claims. At the time of or after your visit, you may pay a copay. The doctor's billing department will then fill out a health insurance claim form to determine whether you owe more money.

Most people only get involved in the claims process if their company denies their claim or insurance only covers a portion of the costs. At this point, you can appeal the decision if you feel your plan should cover the services.

Life insurance claim

Life insurance pays your beneficiaries after they send a copy of your death certificate to the insurance company.

People usually get life insurance to help their family with daily living expenses, college tuition and funeral expenses after they're gone.

What does it mean to file an insurance claim?

Filing an insurance claim means you let your insurance company know about a loss and request that it pay the associated costs. You'll typically have to fill out a "proof of loss" form to file a claim.

Insurance claim definition

An insurance claim is a request you file with the insurance company asking it to pay for a covered loss.

Many companies allow you to file a claim online, through an app or over the phone.

When filing an insurance claim, you almost always pay a deductible before getting a check from the insurance company.

How to make a claim

Filing an auto or homeowners insurance claim is a multi-step process. Not all claims follow the same order or schedule. The time limit to file a claim varies by state. So it's important to start the claims process as soon as possible.

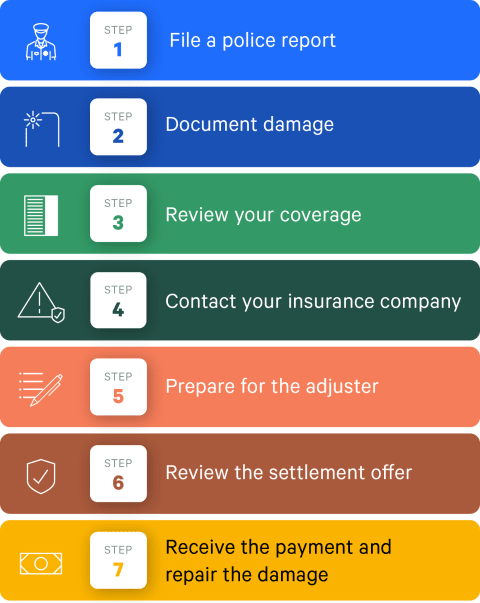

7 steps to file a home or auto claim

Step 1: File a police report

If your claim is for a car accident or any illegal activity , call the police immediately. Don't call 911 unless the situation is urgent. Instead, use your police department's non-emergency line. Depending on your location, you may need to visit the police station to file your report.

Step 2: Document any damage

Next, take time to document the damage properly. You'll need to send photos or videos to your insurance company as proof with your claim.

For car crash claims, take photos or videos of the scene before you move your car, if you can do so safely.

Document property damage claims before you clean up any mess to show your company the full extent of the damage.

Step 3: Review your coverage

Before filing a claim, make sure you understand your coverages, limits and deductibles. Reviewing your policy will help you avoid filing a claim for a loss your company won't cover or one where the cost of the repairs is less than your deductible. Your agent can help you with the process.

Claims that your company doesn't pay may not affect the cost of your insurance. But they will stay on your record.

Making multiple claims in a short period can cause your rates to go up. That's because insurance companies believe you're more likely to make future claims.

Step 4: Contact your insurance company

After determining whether your policy covers the damage, file your claim. Many insurance companies allow you to file simple claims online. For larger claims, contact your agent or call the phone number on your policy.

Before you begin, have all the information about your claim handy. This includes the date of loss, police report, receipts for damaged belongings, medical bills for injuries and any other documents you plan to use to show cost, the damage or proof of fault.

Company | Phone | File a claim online |

|---|---|---|

| Allstate | 800-726-6033 | Start a claim |

| Farmers | 888-327-6335 | Start a claim |

| Geico | 800-207-7847 | Start a claim |

| Liberty Mutual | 800-295-2820 | Start a claim |

| Nationwide | 800-421-3535 | Start a claim |

Step 5: Prepare for the insurance adjuster

Once you've filed a claim, your insurance company will send an adjuster to check out the damage. It's the adjuster's job to determine how much your insurance company will pay.

You may not need to be there during the adjuster's visit. However, walking your adjuster through the damage can be helpful. Speaking with your adjuster will allow you to show them the damage and discuss your claim. You can also ask questions about your policy.

You can expect an insurance adjuster to:

- Inspect your home or vehicle.

- Review your policy to ensure it covers the damage.

- Interview you regarding the incident.

- Request contact info for anyone involved, like doctors, lawyers or witnesses.

You don't need to get repair estimates before meeting with your adjuster, but it can be helpful, especially for large claims. Sharing the quotes with them can give insight into what local contractors or auto shops charge for repairs.

Some businesses have a lot of experience with insurance claims and may even help you through the process.

Step 6: Review the settlement offer

You'll get a settlement offer after your adjuster sends their report to the insurance company. Review the offer carefully, because after you accept it, your claim is closed.

If you're not happy with the offer, you can dispute the claim by asking the company for a second review. You can also hire a public adjuster or attorney.

Step 7: Get the claim payment and repair the damage

Once you've signed the settlement agreement, your insurance company will pay the agreed-upon amount minus your deductible. Then, you can hire a professional to make repairs if your insurance claim involves property damage.

How do insurance companies pay out claims?

The payment process is different for every claim and depends on the type and size of your claim. Smaller claims take less time to process and are more straightforward. You may even get a check from your adjuster on the spot.

When you make a larger claim, you can expect multiple insurance checks throughout the repair process.

Auto insurance settlement

If the cost to fix your car is less than its overall value, your insurance company will send a check to cover the repair bill, minus your deductible. Several factors influence how the payout process works:

- If you own your car outright, the insurance company may send a check directly to you.

- If you have the repairs made at one of your insurance company's preferred auto body repair shops, your company will likely send the check directly to the shop.

-

If you have a lease or loan on your car, the insurance company may make the check out to you and the lender. That's because your loan company is named on your insurance policy.

Your loan company may verify that your car was in an accident and sign the check over to you. Or, it might ask you to sign the check over to the loan company so it can pay the repair company directly.

If the cost to repair your car is more than its current value, your insurance company will consider it totaled. Instead of paying to fix your car, the company will send you a check for the car's pre-accident value.

- If you own your car outright, you can use the check to get a new one. The money is yours, so you can spend it however you like.

- If you have a loan on your car, the insurance check will go toward paying off the rest of what you owe.

Home insurance settlement

Insurance companies pay most home insurance claims with multiple checks. That's because these claims are generally more complex, and repairs take longer.

Sometimes, the insurance adjuster will give you an advance on the total settlement amount at the end of their inspection. This can help you get the repair process started. Accepting this first check doesn't mean you're bound to their initial settlement offer.

If your insurance claim includes damage to the structure of your home, your belongings and additional living expenses, you will usually get separate checks for each category.

Along with paying via multiple insurance checks, the way that companies pay these claims can vary.

-

If you have a mortgage on your home, your insurance company may write checks that cover repairs to both you and the mortgage company. That's because the mortgage company wants to ensure you make the repairs and don't just keep the cash.

Your lender may put the money into an escrow account and pay the contractors directly as they complete the work.

-

The insurance company can send payments directly to your contractor if you sign a "direction to pay" form. It's important that you discuss this with your insurance agent before signing. Some direction to pay forms can assign your entire claim to your contractor. That gives them control over the entire process.

If you choose to have payments sent directly to your contractor, inspect the repair work thoroughly before your insurance company sends the final payment and the claim is closed.

Checks for personal belongings and additional living expenses should only have your name on them.

If you have replacement cost coverage on your belongings, you'll usually get two checks.

- The first check is for the cash value of the damaged items. The cash value is based on their condition before your claim. This is so your insurance company can match the exact cost once you buy replacements. If you decide not to replace the items, you can use this money however you like.

- Once you send the insurance company receipts showing you bought the replacements, it will send the final settlement check. This check is for the difference between the cash value and what you paid for new items.

How long does it take to get an insurance check?

Depending on the amount of damage, settling insurance claims can take anywhere from a few weeks to a few years.

For example, the process may be quick if you were in a car accident and only had minor damage.

However, if you must rebuild your entire home after a fire, the construction may take a few years. In that case, you'll get multiple checks, including an advance upfront to get repairs started.

Can you keep insurance claim money?

If you own your car outright, you can use auto insurance claim money for anything you like. However, your insurance policy won't pay for damage you find later on resulting from the crash if you choose not to make the initial repairs.

You can also use homeowners insurance claim funds however you like, but only if you don't have a mortgage.

Once in a while, you may have home insurance claim money left over after finishing repairs. This money is yours to keep unless your insurance policy says you must return unused funds.

When not to file an insurance claim

Insurance companies keep a record of all claims, whether they pay the claim or not. Not all claims will increase your insurance rates, especially small ones. However, multiple small claims within a short period often raise rates.

Before you file an insurance claim, check your policy to ensure it covers the damage or loss. If you're unsure, call an insurance agent for help.

For small claims, consider whether the cost of fixing the damage or replacing items is higher than your deductible.

For instance, say someone steals your computer and it costs $1,200 to replace. If your deductible is $1,000, filing a claim to get a $200 insurance check may not be worth it.

What happens when someone makes an insurance claim against you?

When somebody makes a claim against your insurance, your company will work to determine whether the accident was your fault.

If you were in a car accident, your insurance company will review police reports and witness statements to determine if you were more than 50% responsible.

If your company decides that you were the at-fault driver, your insurance rates will increase. After an accident, full coverage rates go up by an average of 49% if you don't have accident forgiveness.

If someone is hurt in your home, it's best for you to file a liability claim with your own insurance. This way, you can tell your side of the story and potentially have the claim dropped.

Liability claims are often costly for insurance companies. For that reason, they usually cause a major increase in rates or even policy cancellation.

Disputing a claim

If you aren't happy with your auto insurance claim check, you can dispute the claim. You can do this by contacting your state's insurance department and filing a complaint. Most states have a division that deals specifically with insurance customer issues.

You can also hire an attorney. However, it may cost more than the extra money you could get from the insurance company.

To dispute a home insurance claim or settlement offer, you can start by asking the insurance company to review your claim. If you aren't able to come to an agreement with the insurance company, you can hire a public insurance adjuster.

The adjuster will give you an independent estimate for the damage. Their estimate will either confirm the accuracy of your insurance company's offer or provide evidence you can use to ask for more money.

If a public adjuster believes the insurance settlement is too low and your insurance company refuses to pay more, you can file a complaint with your state's insurance department. You can also hire an attorney.

Frequently asked questions

Can you cancel an insurance claim?

Most insurance companies will allow you to cancel or withdraw a claim as long as you're the person who filed it. The claim will stay on your record but show a $0 payout. It should only affect your insurance rates if you've made multiple claims over a short period.

How soon can you file a claim after getting insurance?

You can file an insurance claim as soon as your policy becomes active. However, the accident must happen while the policy is in effect.

For example, you can file a claim if you get in a car accident on the same day your insurance policy becomes active. However, if you were in an accident the day before you got your policy, you can't file.

What happens when insurance can't get a hold of the person at fault?

When your insurance company can't contact the driver who caused an accident, it will try to contact their insurance company. If their insurance info isn't available or the other company isn't cooperating, your company will generally cover the claim if you have uninsured or underinsured motorist coverage. This type of claim will not raise your rates.

Can you file a claim with two insurance companies?

There is no law against having two insurance policies that cover a single car or home. However, most policies have an "other insurance clause." This clause states that each policy will only pay for a portion of the damage.

Insurance should make you whole after a loss. This clause ensures you don't make money from an insurance transaction.

Can you get insurance after a claim?

You can get insurance after filing a claim. But, depending on the type and size of the claim you file, the cost of your insurance may go up. After very large claims where you are at fault, your insurance company may choose not to renew your policy at the end of the policy period.

Depending on where you live, insurance companies must give you a 30- to 60-day notice when deciding not to renew your policy. This way you'll have enough time to find a new company.

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.